Nyfronix Blog

Personal Finance

29 articles about personal finance, written by the teams building our apps.

What Is the 24-Hour Rule for Spending? How It Stops Impulse Buys

The 24-hour rule means waiting a full day before any non-essential purchase. Here's why the pause stops impulse buying and how to make it stick.

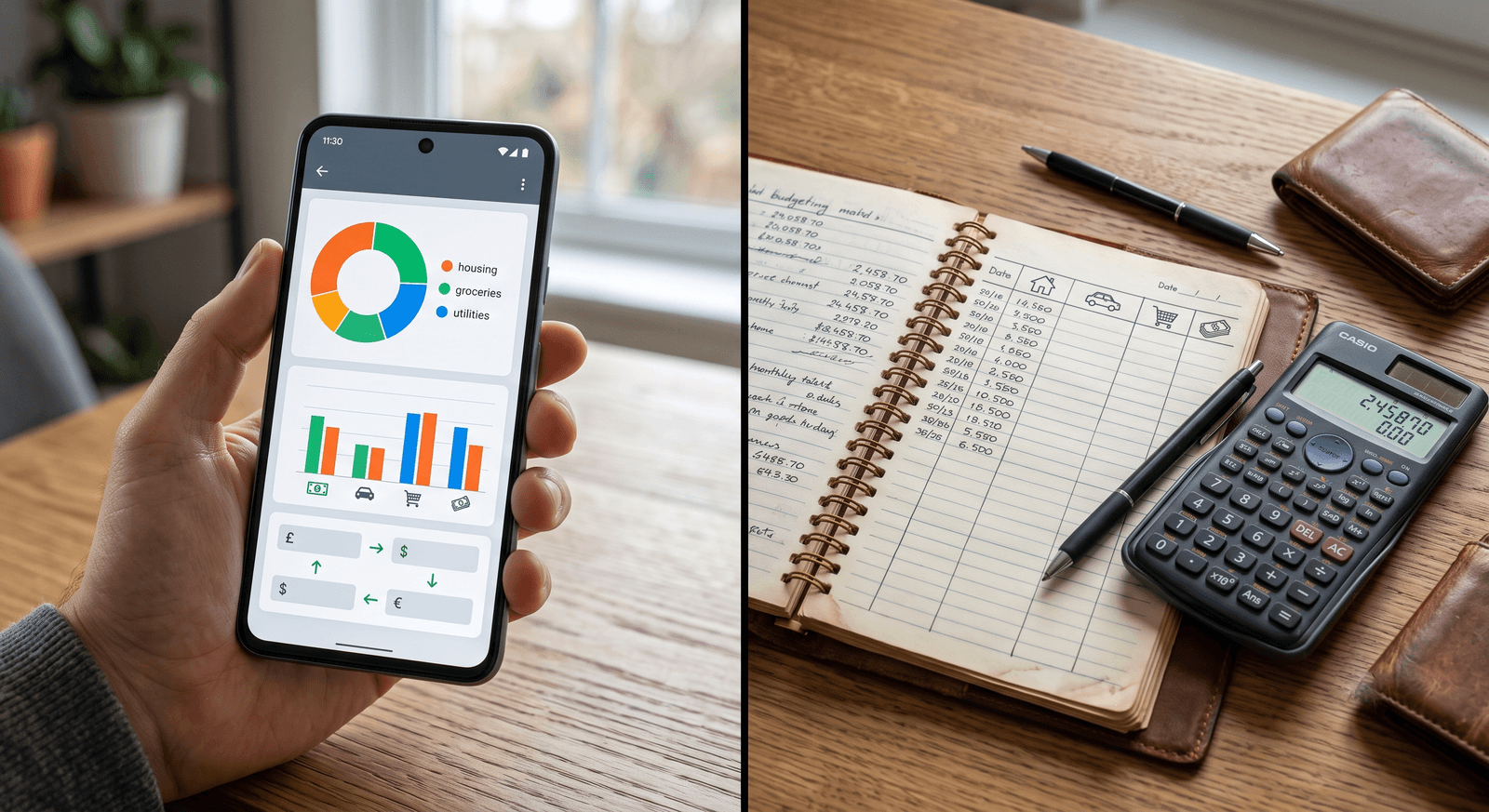

What Is Manual Expense Tracking? A Guide to Budgeting by Hand

Manual expense tracking means recording every expense by hand to monitor spending. Here's how it works, who it suits, and how to start in 3 steps.

What Is Intentional Spending? A Guide to Value-Based Budgeting

Intentional spending aligns your money with your personal values instead of just cutting costs. Here's how it works and how to start.

What Is Impulse Spending? 4 Proven Ways to Stop It

Impulse spending is unplanned buying driven by emotion. Stop it by naming your triggers, using the 24-hour rule, tracking by hand, and adding friction.

What Is Financial Data Privacy? A Comprehensive Guide

Financial data privacy protects your account numbers, transactions, and spending habits. Here's what it covers, the laws behind it, and how to guard it.

What Is a No-Spend Challenge? How It Works and How to Start

A no-spend challenge means pausing all non-essential spending for a set period. Here's how to plan it, avoid pitfalls, and keep the savings after.

What Is a Bank-Linked Budgeting App? How It Works and What It Shares

A bank-linked budgeting app connects to your bank via an aggregator like Plaid to auto-import transactions. Here's how it works and what data it shares.

Mindful Spending vs Mindless Spending: What's the Difference?

Mindful spending is intentional and aligned with your goals; mindless spending is impulsive and unplanned. Here's how to tell them apart and switch.

Bank-Linked vs Manual Budgeting Apps: What's the Difference?

Bank-linked budgeting apps import transactions from your bank automatically; manual apps have you log each expense yourself for privacy and awareness.

Are Budgeting Apps Safe to Use? A Guide to Judging App Security

Most budgeting apps are safe to use. The risk depends on bank access vs manual entry. Here's how to judge encryption, certifications, and monetization.

Zero-Based Budgeting for Beginners: A Step-by-Step Guide

Zero-based budgeting assigns every dollar to an expense, a savings goal, or a debt payment until your budget hits zero. Here's the 5-step process.

Weekly vs Monthly Budgeting: Which One Works Better?

Weekly budgeting suits irregular income with tighter control; monthly suits salaried pay with less upkeep. Trial both to find your fit.

How to Recession-Proof Your Budget: A Practical Guide

Recession-proof your budget with a bare-bones survival budget, a 3-6 month emergency fund, and strategic cuts to discretionary spending.

How to Pay Off Debt When Interest Rates Are High

Pay off debt when rates are high using the avalanche or snowball method, refinance only if it lowers total cost, and track payments by hand.

How Inflation Affects Your Daily Budget (And How to Fix It)

Inflation shrinks buying power, so the same dollars buy less. Track spending, cut costs, and fund needs first to adjust your budget.

Forgotten Subscriptions: How to Stop the Overspending

Forgotten subscriptions can cost you $200+ a year. A manual audit of your statements is the fastest way to find and cancel them.

How to Build an Emergency Fund When Prices Keep Rising

Build an emergency fund during inflation by setting an inflation-adjusted target, automating small transfers, and tracking spending to redirect.

The 50/30/20 Budget Rule Explained: Needs, Wants, Savings

The 50/30/20 rule splits after-tax income into 50% needs, 30% wants, and 20% savings. Here's how to apply and adjust it.

5 Signs You Need to Switch Budgeting Apps (And What to Look For)

Feature bloat, vague privacy, high fees, clunky UX, and no manual entry are the 5 signs to switch budgeting apps. Here is what to look for next.

The Psychology of Spending: How Logging Expenses by Hand Changes Your Financial Habits

Handwriting expenses taps into the 'pain of paying,' boosting spending awareness through loss aversion, present bias, and mood tracking.

Minimalist Personal Finance Tools: Fixing Spreadsheet Burnout

Spreadsheet burnout comes from setup fatigue and missed updates. Minimalist personal finance tools fix it by tracking only what matters.

The Envelope Method Reimagined for the Smartphone Era

Digital envelope budgeting works if you log every expense by hand instead of syncing your bank. Here's how to set it up on your phone.

Automated vs. Manual Budgeting: Which Gives More Financial Control?

Automated budgeting saves time, manual budgeting builds spending awareness, and a hybrid approach offers the best financial control for most people.

How to Adjust Your Budget for Inflation and Rising Interest Rates

Adjust your budget for inflation by prioritizing groceries, utilities, and debt, then reallocating funds and reviewing costs weekly instead of monthly.

Why Manual Expense Tracking Is the Secret to Actually Saving Money

Manual expense tracking creates awareness and cuts impulse purchases through cognitive friction and active recall. Here's why it works, and how to start.

What Happens to Your Data When You Connect Your Bank to an App: A Comprehensive Guide

When you link your bank to an app, tokenization and aggregators like Plaid handle the data exchange. Here's exactly what happens, and how to control access.

Budgeting Apps That Don't Require Bank Access: A 2026 Guide

Manual budgeting apps like Wizpend let you track spending and build budgets without linking your bank account. Here are the best privacy-first options in 2026.

Is It Safe to Link Your Bank Account to a Budgeting App? A Comprehensive Guide

Linking your bank account to a budgeting app can be safe when it uses OAuth. Here's how to judge an app's security, data sharing, and safer alternatives.

The 50/30/20 Budget Rule: How to Split Your Income (With Examples)

The 50/30/20 rule splits your after-tax income into 50% needs, 30% wants, and 20% savings. Here's how to set it up, with real examples.